Millions of American homeowners would love to move — if they could pack up the mortgage interest rate they locked in at under four percent.

“We hate the area we moved to but cannot justify moving again due to mortgage rates,” says Ben Young, who bought in 2021 at a 2.25 mortgage interest rate.

The post-COVID rate crater saw millions of mortgages written or refinanced at historically low interest rates. Homeowners holding onto that 2.8 percent interest rate will be hard to dislodge from their current digs. Staying put often makes sense for individual families, at least financially, but both housing markets and labor allocation are suffering as a result.

Rates for 30-year mortgages remain well below historic averages, but they’ve almost doubled in the past three years, right alongside the Federal Reserve’s interest rates. The psychological impact of that sticker shock is significant. After underestimating the inflationary damage its post-pandemic loose money would generate, the Fed overcorrected with historically quick monetary tightening, raising rates 11 times since spring 2022. The average interest rate on a 30-year fixed mortgage inched above six percent in September 2022 and has stayed there. Anyone who locked in a low rate then is thinking twice about giving it up now.

Insurance, property taxes, and cost of living all impact monthly expenses for homeowners, and in some cases dwarf the interest rate differential. But for many, and certainly psychologically, giving up a guaranteed low mortgage payment is difficult.

David and Sarah Veksler welcomed a third child this year, but upgrading their home in Denver feels daunting. “Definitely feeling stuck here,” he told me. “We have a new baby boy and he’s waiting for rates to go down before he can get his own room. He’ll have to share with his sisters until then.”

Individually rational choices, in aggregate, are causing a huge problem. Even if they didn’t buy, millions of homeowners refinanced during the low-rate years. By spring of 2022, 92.8 percent of homeowners had a mortgage rate under six percent. Six in ten homeowners still have a mortgage below four percent.

Fixed-rate mortgages are actually adjustable, thanks to the ready availability of refinancing options, but only in one direction. Borrowers refinance to lower their payments, so rate adjustments are almost exclusively downward. When a buyer refinances, generally speaking, the new bank issues a new mortgage and pays off the original mortgage. The original lender receives back the principal to lend at 7 percent, instead of waiting for a 30-year mortgage to trickle in at the now-paltry 2.8 percent. As with other voluntary transactions, all parties benefit.

A low mortgage rate is highly desirable, and non-transferable. Once “locked in,” a comparatively low mortgage rate functions as an emotional and economic anchor. Homeowners are less likely to step up the property ladder (vacating their starter home for a larger one, or a more desirable school district), and also less likely to downsize and move on when their needs change. Both the supply (existing homes entering the market) and the demand (people searching for a new one) are suppressed by mortgage rate lock-in. The property market stagnates.

This helps explain why, as of August 2024, the inventory of homes for sale in the US remains 38 percent off its July 2016 peak and 26 percent below where it was in August 2019.

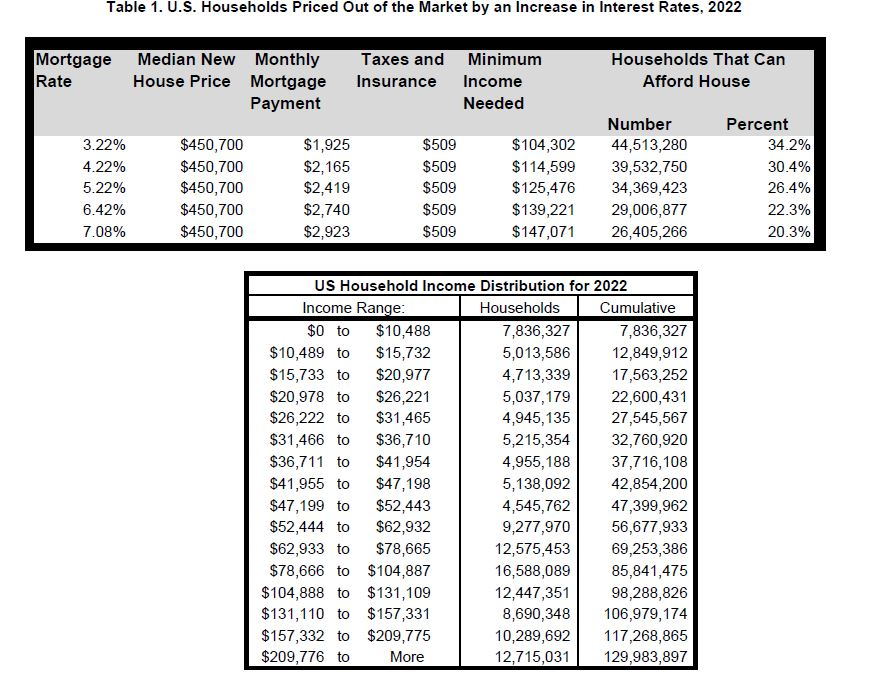

How high are the costs of mortgage lock-in? According to research by economists Jack Liebersohn and Jesse Rothstein, a 2.7-percentage-point rate gap between locked in and prevailing interest rates raises the average mortgage balance – the ‘price’ of moving – by $49,400. Na Zhao, economist with the National Association of Home Builders, found that a rise in prevailing mortgage rates of 100 basis points increases the annual income required to qualify for a loan by $10,000. Each such bump (from a 4.0 interest rate to 5.0, or 5.5 to 6.5) “prices approximately five million additional households out of the market for a home at the same or similar price level.” Just one in five American families earns enough to qualify for median-priced homes at seven-percent interest.

In a turbulent economic time, moving presents a major cost that can be avoided entirely by riding out at least another few years at a locked-in pandemic fire-sale rate. Homeowners facing those incentives are more likely to stay put.

Data confirm mobility declines as mortgage rates rise. Liebersohn and Rothstein calculated that rate lock discouraged 660,000 moves in 2023, a deadweight loss to the economy of $17 billion that year.

Mortgage Lock-In Reduces Labor Mobility

As the property market locks up, labor mobility does, too. Someone who bought a typical home at a typical rate in 2016 (3.5 percent) would pay almost 40 percent more each month, if they were to take out a fresh mortgage on an identical home at the now-common rate of around 7 percent. One study placed the annual increase in mortgage payments at $5,000 when moving to a roughly equivalent new home, but given the rising price of homes and property taxes, that’s likely conservative.

Researchers Julia Fonseca and Lu Liu report, “mortgage lock-in modulates the geographical allocation of labor and leads to a mismatch between workers and jobs, as some households forego higher-paid employment opportunities due to the financial cost imposed by mortgage lock-in.” Locked-in households were half as likely to move in response to potential wage growth.

The favorable difference in pay or cost of living must be commensurately larger to entice someone to seize her potential by moving to a new city, or even across town. Another finger on the scales: locked-in mortgage rates are less likely to transfer into or out of self-employment, and the availability of work-from-home jobs may also make people less likely to move.

International Alternatives

Other countries have experimented with ways to alleviate lock-in. In the United Kingdom and Canada, many mortgages are portable, meaning you can essentially transfer your mortgage terms from an existing property to a new one. Americans, in general, secure a mortgage for a particular property and must start over, with a new interest rate and repayment terms, to purchase a subsequent one. Other international mortgages are assumable, meaning you can sell your mortgage, with its favorable low rates, to a buyer along with the property. Individual owner-occupants must qualify under the original lending terms. Where do we find assumable mortgages in the United States? Among those issued by the Federal Housing Administration (FHA), the Department of Veterans’ Affairs (VA) and some Department of Agriculture (USDA) loans.

The complex web of regulation surrounding home-lending put these options off limits for most Americans, or at least those buying without the help of the federal government. The Federal Housing Finance Agency, on behalf of Fannie Mae and Freddie Mac, told The New York Times and American Banker earlier this year that portable mortgage options “are not under consideration” for the general public. The Times concluded, “Right now by law there’s no way to detach that loan from the property that serves as its collateral and reattach it to a new property.”

Rapid changes in mortgage rates cause homeowners to stay put, and the housing and labor markets suffer the consequences. People are less likely to move, either to bigger homes or to better jobs, stagnating economic mobility. While other countries have found creative, free-market solutions to reduce the impact of mortgage lock-in, America’s complex regulatory environment keeps these options out of reach for most buyers.

Portability has its own peculiarities, like shorter lending terms and high qualification criteria. Portability and assumability also post major risks for investors who buy securitized mortgages. Powerful interest groups, including financial institutions who currently impose their own terms and mortgage brokers who profit from underwriting and replacing each reissued mortgage, also play a role in maintaining the status quo. Giving Americans a freer mortgage market with more choices might benefit the economy, but would take a major lobbying push.

Mortgage lock-in is just one more example of the inevitable, if unintended, consequences of asking the Federal Reserve (or any other group of mortals) to exercise discretion in these macroeconomic matters. The Federal Reserve has just cut the rate by 50 basis points and is expected to make another cut before December, but homeowners will continue to feel locked into their mortgages — and the broader economy will continue to feel the strain created by recent, artificially low rates. Until then, we can expect fewer “For Sale” signs and more “Stay Put” decisions, as financial incentives restrict economic mobility.

The post Stay Put or Pay Up: Why Can’t Your Mortgage Move With You? was first published by the American Institute for Economic Research (AIER), and is republished here with permission. Please support their efforts.